How to Purchase Reverse Mortgage and Maximize Your Home’s Value

How to Purchase Reverse Mortgage and Maximize Your Home’s Value

Blog Article

Unlock Financial Flexibility: Your Overview to Investing In a Reverse Home Loan

Recognizing the intricacies of reverse mortgages is important for homeowners aged 62 and older looking for monetary liberty. As you consider this choice, it is critical to realize not just just how it works but also the effects it might have on your economic future.

What Is a Reverse Mortgage?

The essential allure of a reverse home mortgage depends on its prospective to boost financial flexibility during retirement. Property owners can make use of the funds for various functions, consisting of medical expenditures, home enhancements, or daily living costs, thus supplying a safety and security internet throughout a critical phase of life.

It is important to understand that while a reverse mortgage allows for boosted capital, it additionally reduces the equity in the home in time. As interest gathers on the exceptional lending balance, it is vital for potential debtors to thoroughly consider their long-term financial plans. Consulting with a reverse home mortgage or an economic advisor specialist can offer valuable understandings right into whether this option lines up with an individual's economic goals and scenarios.

Qualification Needs

Comprehending the qualification requirements for a reverse home mortgage is important for homeowners considering this economic option. To certify, candidates should be at the very least 62 years old, as this age requirement enables seniors to access home equity without monthly home loan settlements. Furthermore, the property owner has to occupy the house as their main residence, which can include single-family homes, specific condos, and manufactured homes fulfilling certain guidelines.

Equity in the home is an additional crucial need; homeowners generally need to have a considerable quantity of equity, which can be figured out through an appraisal. The amount of equity offered will straight affect the reverse mortgage amount. Moreover, candidates have to demonstrate the capability to maintain the home, consisting of covering building taxes, property owners insurance coverage, and upkeep expenses, making certain the home continues to be in great problem.

Additionally, possible borrowers should undergo an economic evaluation to assess their revenue, credit score background, and general economic situation. This analysis assists lending institutions establish the candidate's ability to meet recurring commitments associated to the property. Fulfilling these needs is important for protecting a reverse home loan and making sure a smooth financial change.

Benefits of Reverse Mortgages

Numerous benefits make reverse mortgages an attractive alternative for elders looking to improve their economic versatility. purchase reverse mortgage. One of the primary advantages is the ability to convert home equity into money without the demand for month-to-month home loan payments. This attribute allows seniors to gain access to funds for numerous demands, such as clinical expenses, home improvements, or daily living expenses, therefore easing economic stress and anxiety

In addition, reverse home mortgages give a safeguard; seniors can remain to live in their homes for as long as they satisfy the financing requirements, cultivating stability during retirement. The profits from a reverse mortgage can additionally be utilized to postpone Social Security benefits, possibly leading to greater payments later.

In get redirected here addition, reverse mortgages are non-recourse fundings, suggesting that consumers will never owe more than the home's reference worth at the time of sale, securing them and their successors from financial responsibility. Finally, the funds received from a reverse home loan are normally tax-free, including one more layer of economic relief. In general, these advantages placement reverse home mortgages as a useful option for seniors seeking to improve their economic scenario while maintaining their treasured home environment.

Charges and costs Entailed

When thinking about a reverse home loan, it's crucial to know the numerous prices and costs that can affect the overall monetary picture. Understanding these expenditures is vital for making an informed choice regarding whether this monetary item is ideal for you.

Among the main prices linked with a reverse mortgage is the source charge, which can differ by loan provider yet generally ranges from 0.5% to 2% of the home's assessed value. In addition, home owners need to expect closing prices, which might consist of title insurance coverage, appraisal fees, and credit record fees, normally totaling up to a number of thousand bucks.

Another substantial expenditure is home loan insurance coverage premiums (MIP), which safeguard the loan provider versus losses. This charge is normally 2% of the home's value at closing, with a continuous yearly premium of 0.5% of the remaining funding equilibrium.

Last but not least, it is essential to think about ongoing costs, such as property tax obligations, house owner's insurance, and upkeep, as the debtor remains liable for these expenditures. By very carefully examining these costs and prices, homeowners can much better assess the monetary ramifications of seeking a reverse mortgage.

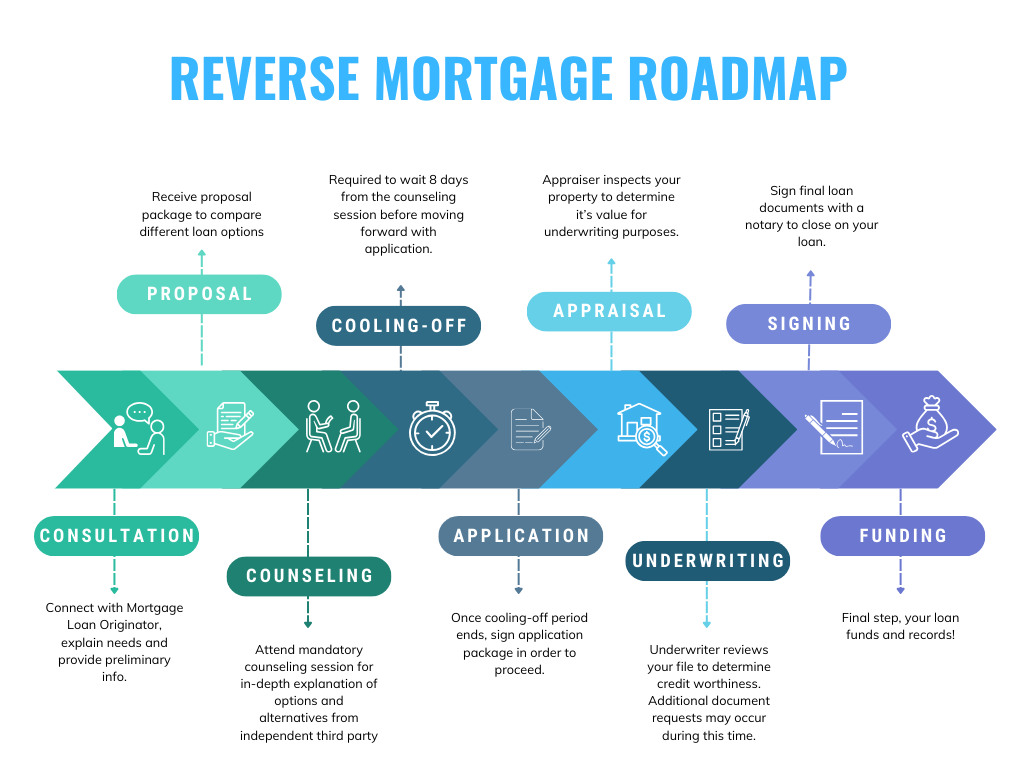

Steps to Begin

Beginning with a reverse home loan includes several crucial steps that can help enhance the process and guarantee you make notified choices. Examine your financial circumstance and identify if a reverse home mortgage lines up with your long-lasting objectives. This includes reviewing your home equity, present financial debts, and the need for extra revenue.

Next, research study numerous lending institutions and their offerings. Try to find respectable institutions with favorable testimonials, clear charge frameworks, and affordable rates of over at this website interest. It's vital to compare conditions and terms to find the most effective fit for your requirements.

After choosing a loan provider, you'll need to finish a thorough application procedure, which normally calls for paperwork of earnings, properties, and residential or commercial property information. Take part in a therapy session with a HUD-approved counselor, who will supply understandings into the implications and responsibilities of a reverse home mortgage.

Verdict

In verdict, reverse home loans offer a viable option for elders seeking to enhance their economic stability during retirement. By converting home equity right into available funds, house owners aged 62 and older can attend to various financial requirements without the pressure of month-to-month payments.

Recognizing the complexities of reverse home mortgages is important for homeowners aged 62 and older seeking economic flexibility.A reverse home mortgage is an economic item developed largely for property owners aged 62 and older, allowing them to transform a section of their home equity right into cash money - purchase reverse mortgage. Consulting with a reverse home loan or an economic expert expert can supply important understandings right into whether this option straightens with a person's financial goals and scenarios

In addition, reverse home mortgages are non-recourse car loans, indicating that consumers will certainly never ever owe more than the home's worth at the time of sale, securing them and their successors from monetary responsibility. Generally, these benefits position reverse home mortgages as a practical service for senior citizens looking for to improve their financial scenario while maintaining their valued home setting.

Report this page